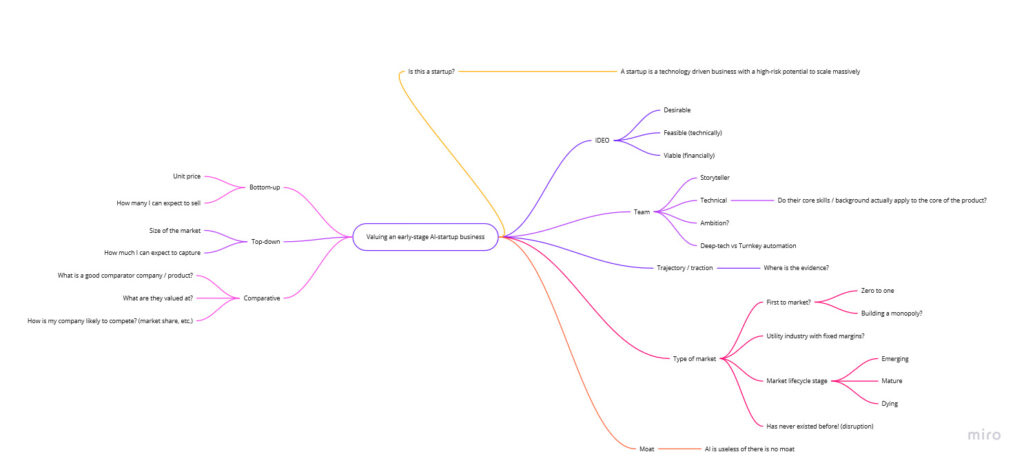

I had an interview recently in which I was asked how I value an early-stage startup. The following mind-map was my answer.

The first question is, is this a startup? People in government funding agencies like to dispute definitions so I want to be clear, I’m only talking about companies – typically involving a technological approach – with a high-risk potential for enormous growth.

Then I take the IDEO three lenses approach to product innovation. Is the solution desirable, feasible and viable. And what is the evidence for each?

How to the team look? When I began founding, team was the only thing I was interested in. Working with German investors pushed me off that topic for a while – they don’t care about team, they want a turnkey solution for profitability (i.e. they are not VCs). But I subsequently returned to my roots. With a poor team you might build a business, but you will not build a high-return entity. You need the best.

Are the team ambitious? Is there a good storyteller amongst them? To what degree is this a deep-tech vs direct execution startup? And on the technical side, does the background of the technical partner(s) line up with the product needs? An MIT degree is great, but not if it’s in the wrong topic.

Trajectory and traction are of course the best indicators. However, these are hard to measure at an early-stage, and talented founders control the information flow to appear to have generated sudden traction, when actually it’s the work of years and mommy and daddy’s best efforts.

What kind of market is the startup in? Peter Thiel has described the zero to one phenomenon. Will they be first to market? Is this a likely monopoly marketplace? Let’s not forget that it’s usually third to market who, improving upon the mistakes of others, holds the terrain. Where are we in the market lifecycle? Early – mature – late? Is this product a potential disruption? In the latter case then a lot of metrics are upended.

Finally, a company needs a moat. Unless you are a me-too product, entering an already crowded marketplace – in which case venture funding is inappropriate – you should have some form of theoretical moat.

On the left-hand side of the map I summarise the three primary methodologies for actually pricing the startup / market. Bottom-up numbers are built upon unit prices and sales forecasts. Top-down are based upon how much of the market you can capture. And comparative numbers are derived from analogy to companies with similar products or similar strategies, often in a different field.

[This article is part of the Innovation Snippets series]